How wine-backed lending works.

Each loan is aligned with your objectives through a structured, relationship-led process that combines asset assessment, credit discipline, and secure collateral management.

At a glance

The Jera approach, summarised.

Five things to know about borrowing against wine.

Low-friction enquiry

No full wine list required upfront. Start with collection value, storage location, and desired loan size.

Specialist valuation

Proprietary modelling supported by Liv-ex data, Wine-Searcher and direct market knowledge, focused on realisable value.

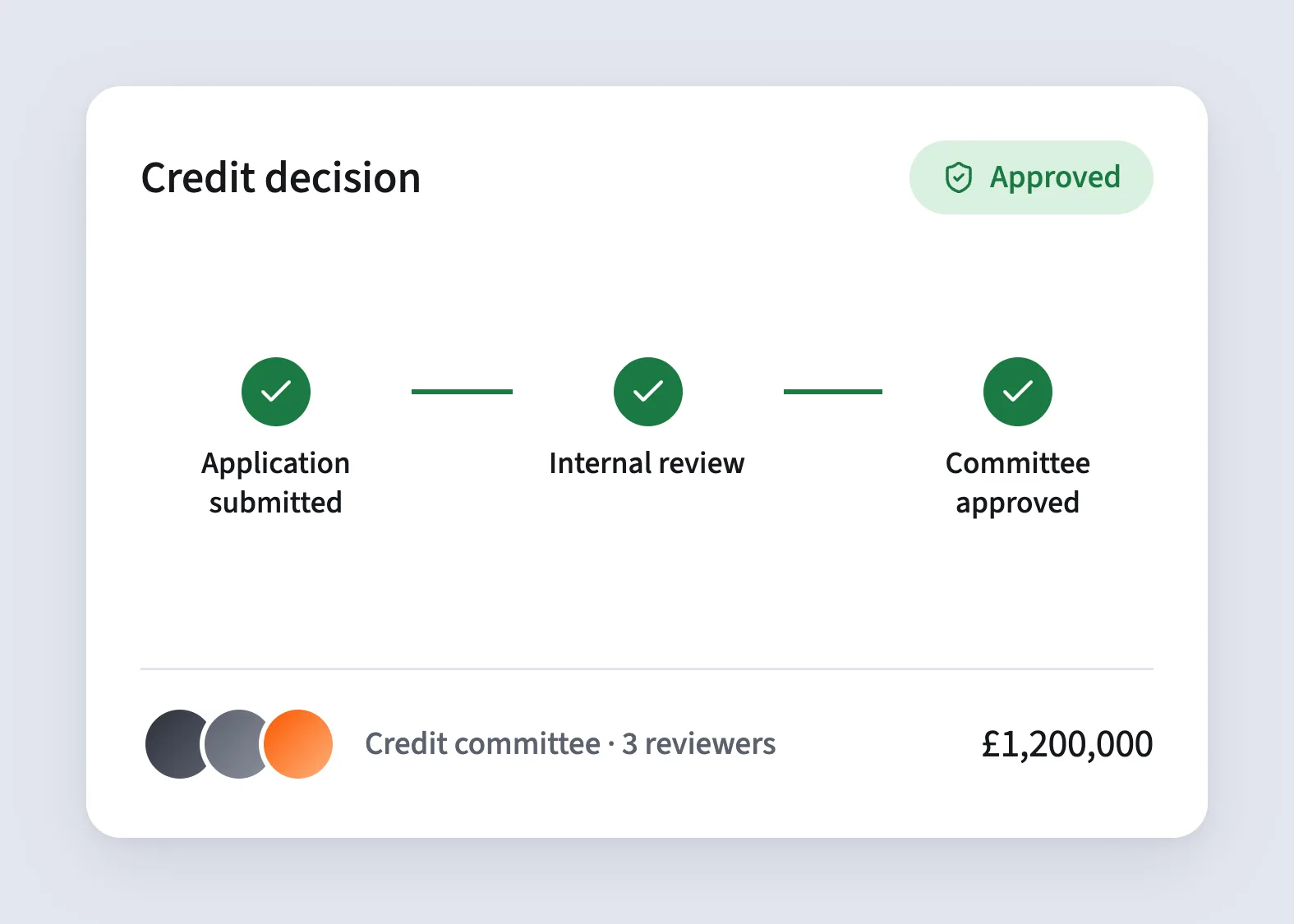

Structured credit

Formal internal review and approval, with loans typically structured at 50–60% loan-to-value over 1–3 years. Interest typically 10–12% per annum.

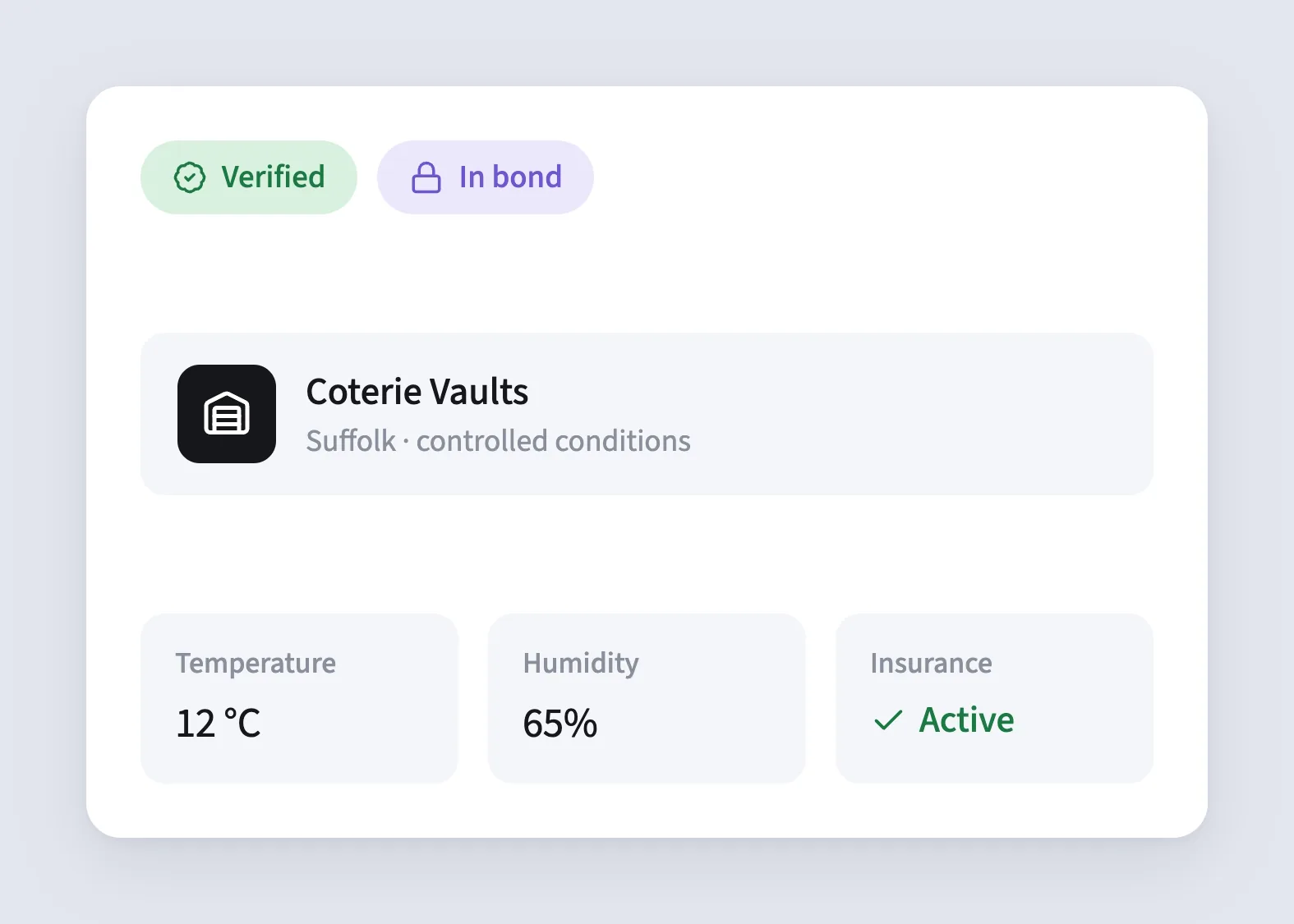

Secure collateral

Wine held in approved bonded storage. Climate-controlled, monitored, insured, and verified on intake.

4-6 weeks to Funding

Typical time from initial enquiry to funds released, with a consistent point of contact throughout.

The process

From enquiry to funds released.

The early steps are simple and low-commitment, with detail and verification introduced as the facility takes shape.

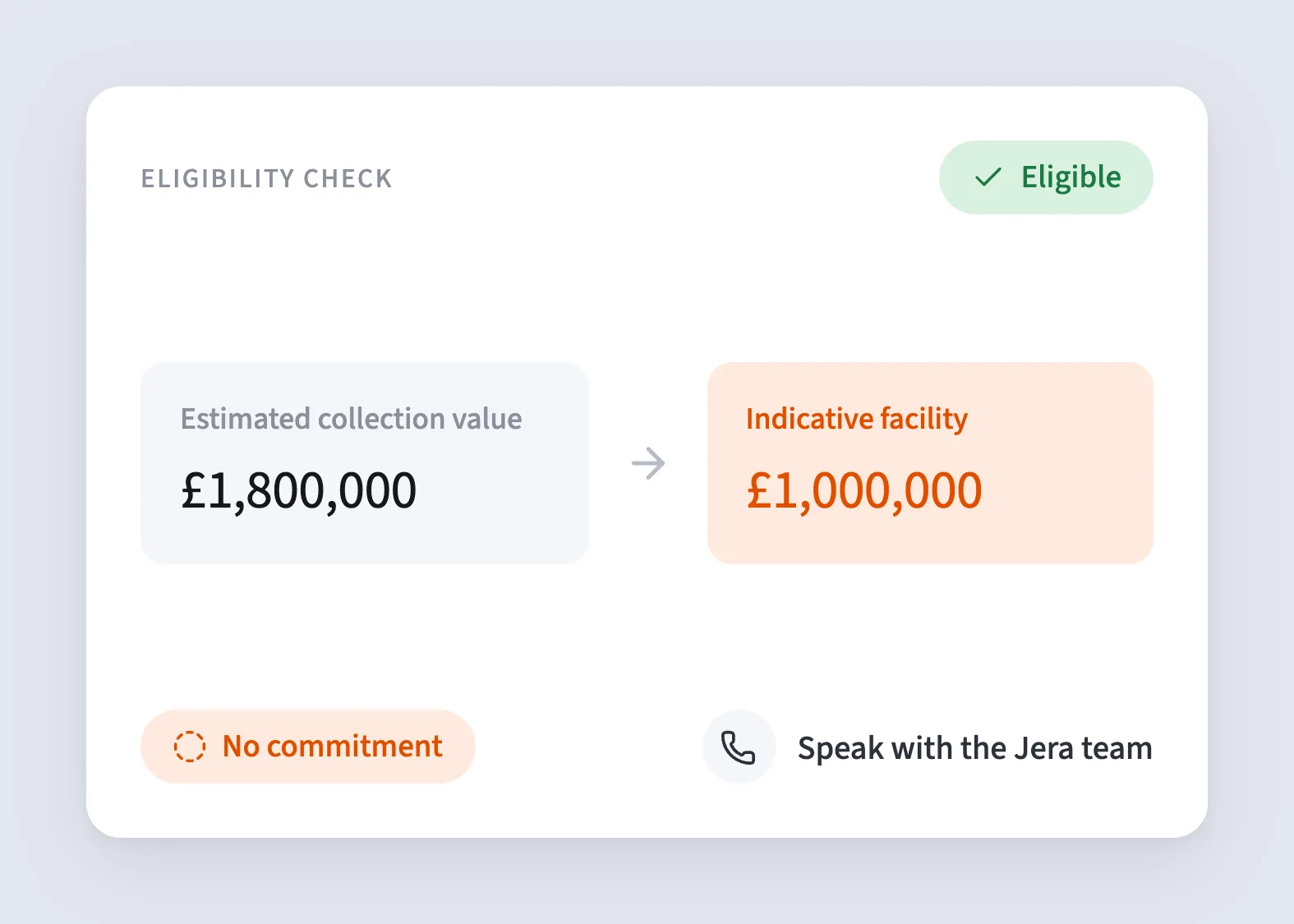

01

Initial enquiry

You complete a short eligibility check or speak with the Jera team to outline your requirements. No commitment at this stage. Just a starting conversation.

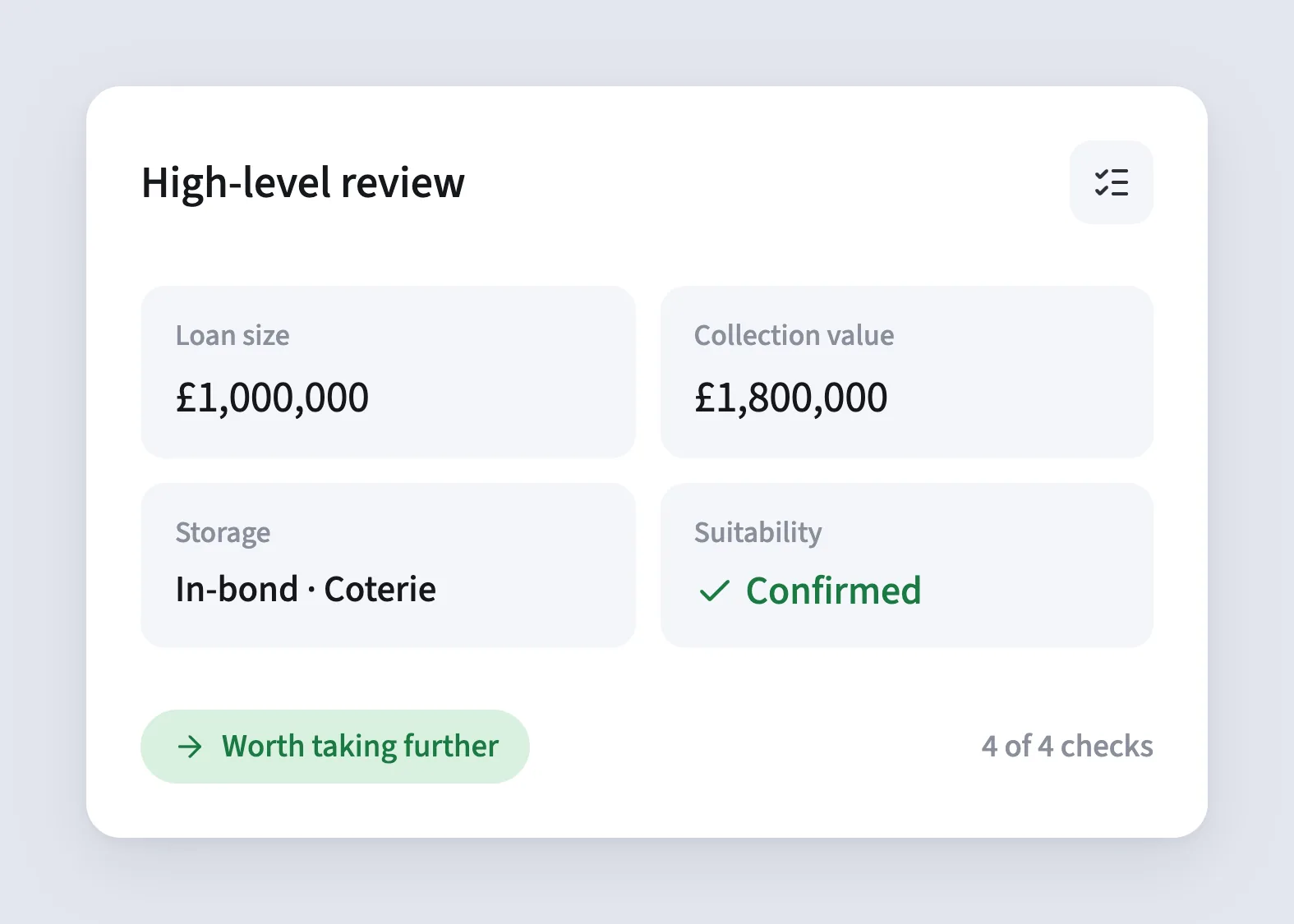

02

High-level assessment

We review key details such as loan size, collection value, storage location, and overall suitability. Enough to confirm the opportunity is worth taking further.

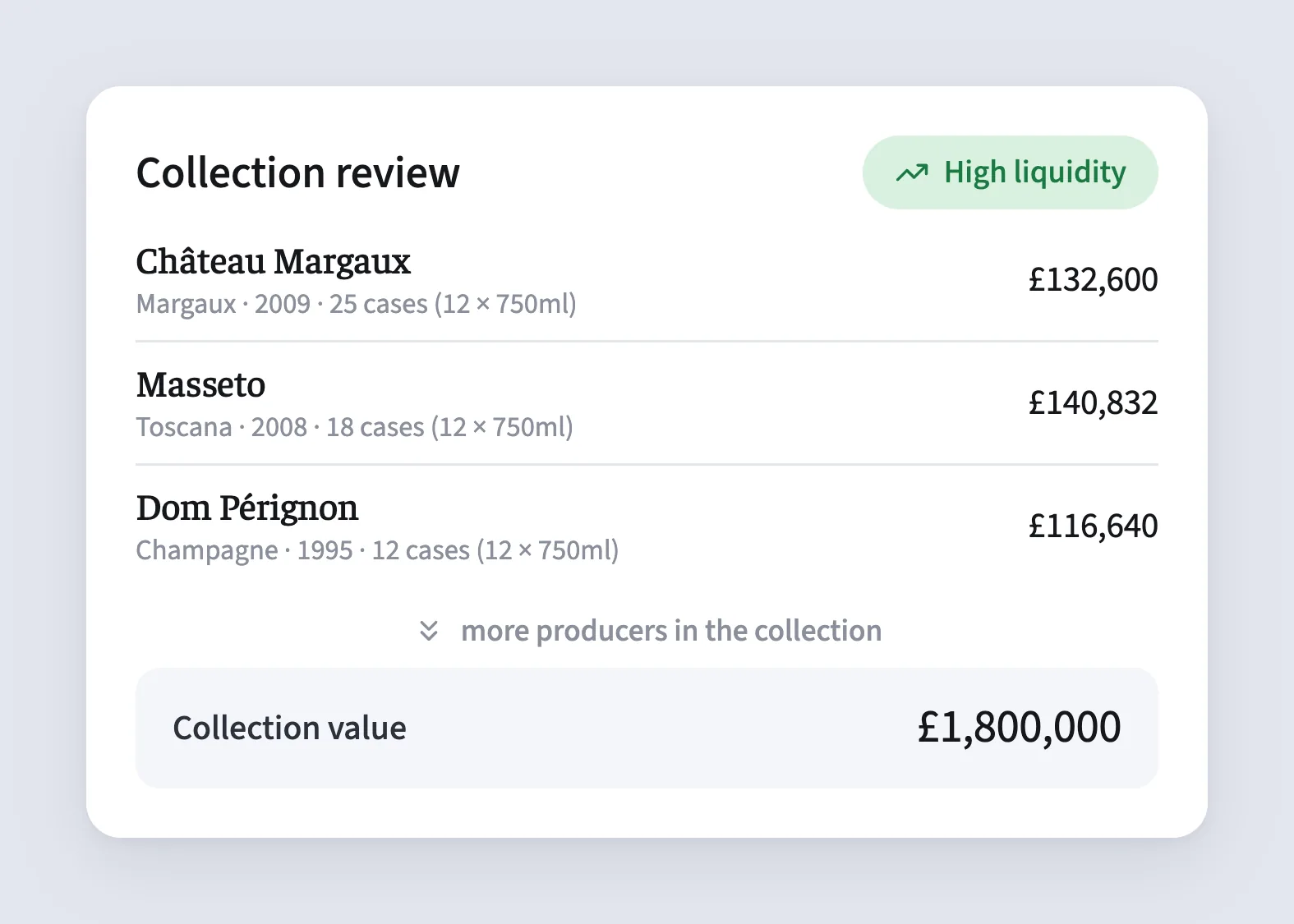

03

Collection review

If suitable, we assess the composition, quality, and liquidity of the collection in more detail. Producers, vintages, volumes, and market demand.

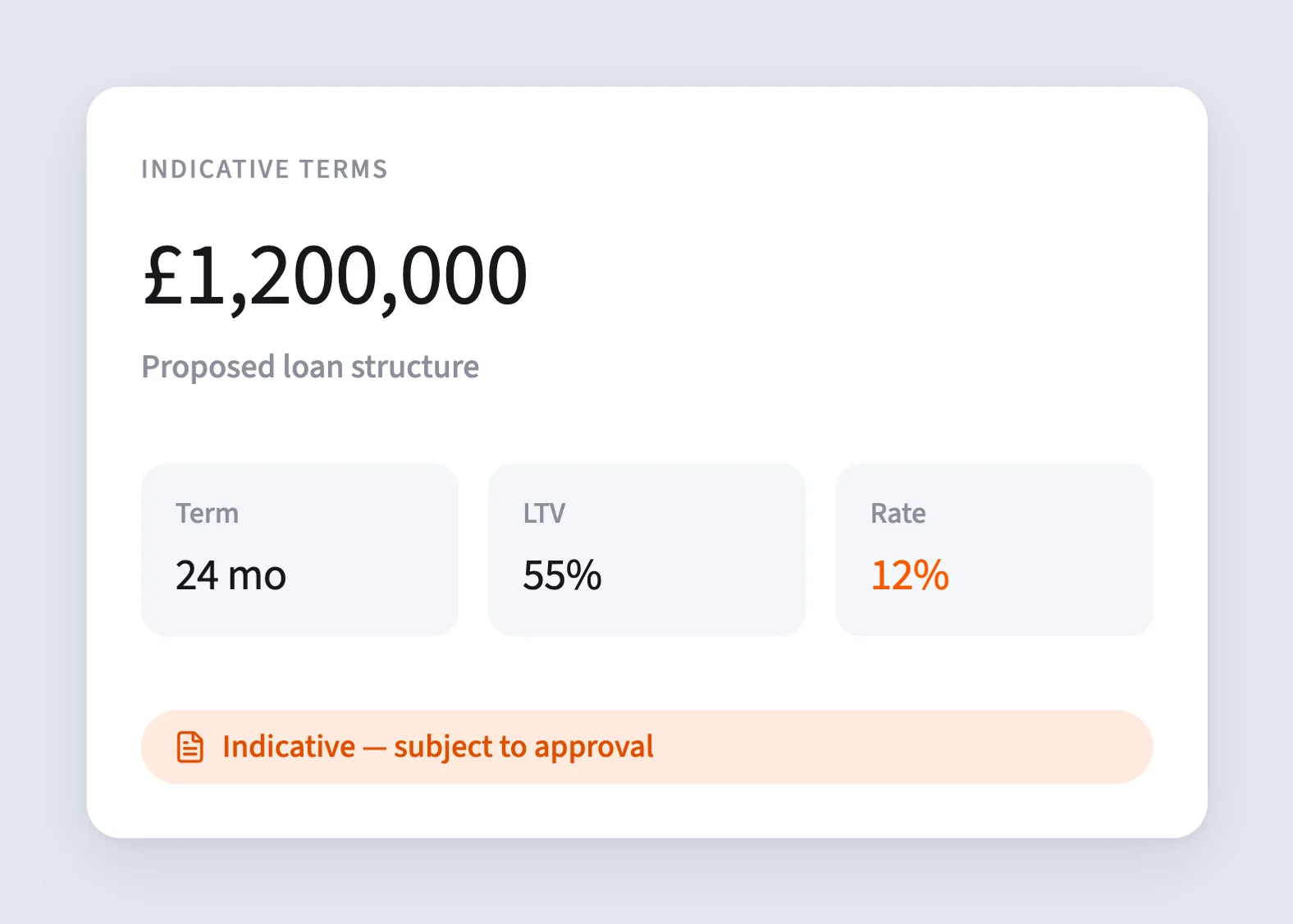

04

Loan structuring

Indicative loan terms are developed based on the realisable value of the collection and your objectives including facility size, term, and structure.

05

Credit approval

Each facility is subject to a structured credit process, including internal review and formal approval. Disciplined and supported by the underlying asset.

06

Collateral arrangement

The wine is verified, inspected if required, and held in approved storage under controlled conditions for the duration of the facility.

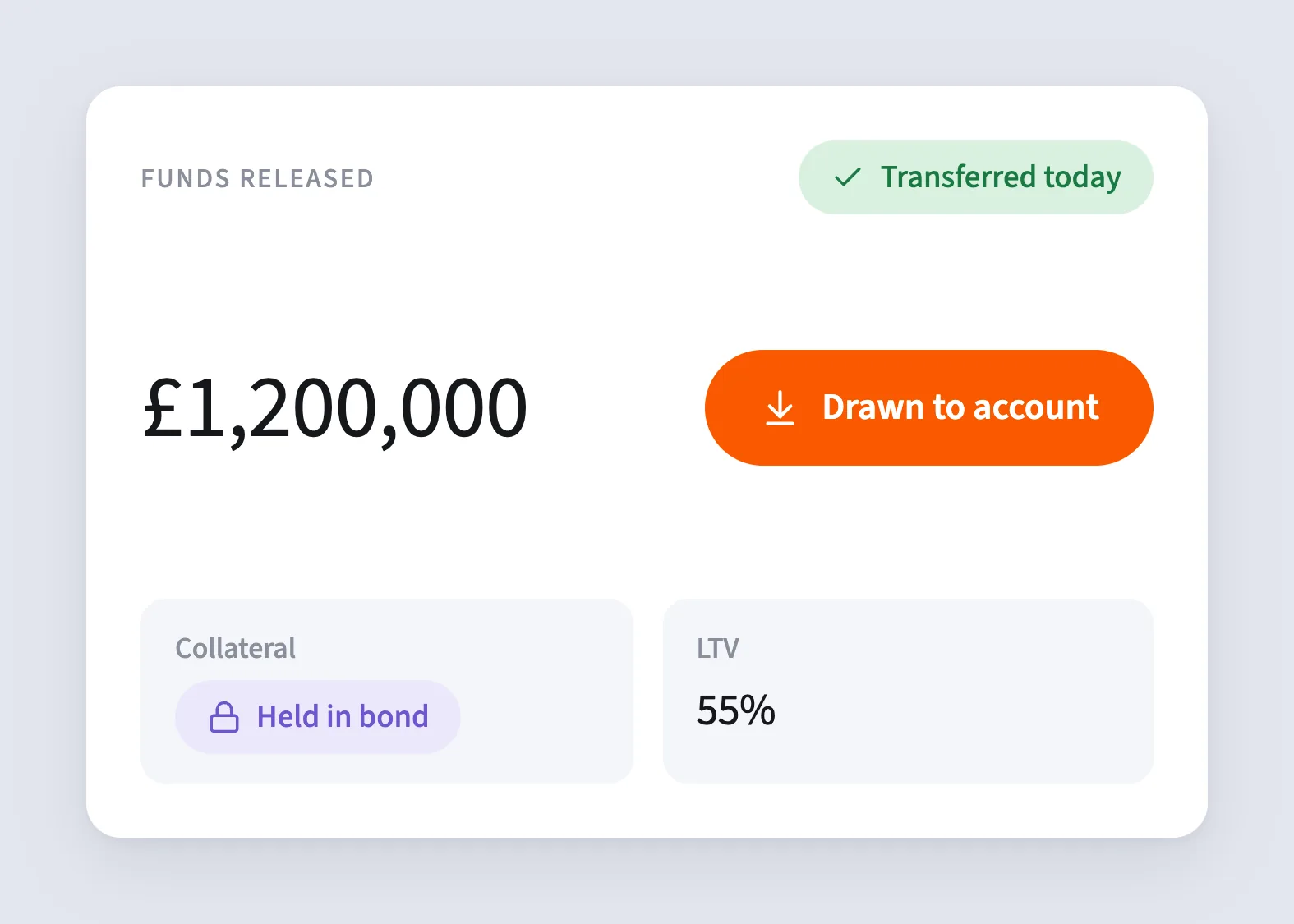

07

Funding

Once all arrangements are in place, funds are released to your account. The wine continues to be held as collateral until the loan is repaid or refinanced.

Valuation

Understanding the realisable value of your collection.

Valuations combine live trading data, historical pricing, proprietary modelling and specialist wine expertise to assess quality, liquidity and market demand.

The objective is not simply to estimate value, but to determine how reliably the collection can support a lending facility.

Storage

Secure collateral. Continued ownership.

Your wine serves as collateral for the duration of the loan, while ownership remains with you throughout.

Collections are held in approved bonded warehouses or professional storage facilities, providing the security, verification and environmental controls required to protect the integrity of the asset.

During & after the loan

From drawdown to repayment.

Once funds are released, your collection remains professionally managed while continuing to support the facility.

At the end of the term, the loan can typically be repaid, refinanced or settled through the sale of the collection, with any surplus value returned to you.

FAQ

The process, explained.

Common questions about the journey from enquiry to funding. Full answers on the FAQs page.